Wazir-e-Azam Apna Ghar Program

Wazir-e-Azam Apna Ghar Program In Pakistan, owning a house has always been a lifelong goal for most families, yet for many people this dream remains out of reach due to rising property prices and limited savings. Over the past few years, the gap between income and housing costs has widened, especially in urban areas, where rent consumes a major portion of monthly earnings. This is where the Wazir Azam Apna Ghar Program 2026 under the “Ghar Ho Tu Apna” initiative becomes highly relevant. It is not just another government announcement; it is a structured effort to turn tenants into homeowners.

اپنا گھر لون رجسٹریشن

آپ کا ڈیٹا چیک کیا جا رہا ہے…

5

مبارک ہو!

آپ کی درخواست موصول ہوگئی ہے۔ ہم آپ کو آفیشل پورٹل پر ری ڈائریکٹ کر رہے ہیں۔

From what I have observed on the ground, many people are unaware of how such schemes actually work. They hear about loans and assume the process is complicated or risky. This program, however, has been designed to remove that fear. It offers a simplified, transparent, and accessible path toward home ownership, making it easier for ordinary citizens to understand and apply without needing expert knowledge.

Understanding the Ghar Ho Tu Apna’ Housing Initiative

The “Ghar Ho Tu Apna” program is essentially a government-backed housing finance scheme that supports individuals through subsidized loans. The key idea behind this initiative is to reduce the financial burden by offering a low markup rate and sharing risk with banks. This encourages financial institutions to lend to individuals who may otherwise be considered high-risk borrowers.

In simple terms, the government steps in to make loans affordable and accessible. Instead of facing high interest rates and strict conditions, applicants benefit from reduced markup and flexible repayment options. This approach is especially helpful for salaried individuals, daily wage earners, and small business owners who often struggle to secure housing loans from traditional banking channels.

Key features of the program include:

- Government-supported subsidy on markup

- Risk-sharing mechanism with banks

- Focus on low and middle-income groups

- Transparent and simplified application process

Who Can Apply? Eligibility Criteria

The program is focused on first-time homebuyers, making the rules simple and clear:

- Must be a Pakistani citizen with a valid CNIC.

- Must not already own a house or flat in Pakistan.

- Open to government employees and the general public.

- Residents from all regions of Pakistan, urban or rural, are eligible.

By keeping eligibility straightforward, the program allows maximum participation and ensures that those who need housing the most can benefit

Major Benefits of Apna Ghar Loan Scheme

One of the strongest aspects of this scheme is its affordability. Unlike conventional loans where high interest rates make repayment difficult, this program offers a structured plan that keeps installments within reach. In the early years, when financial pressure is usually highest, borrowers benefit from a fixed and low markup rate, which provides stability and predictability.

Another important benefit is flexibility. The scheme allows individuals to choose how they want to use the loan, whether for buying a house, constructing one, or even purchasing a plot and building later. This flexibility ensures that people from different backgrounds can benefit according to their needs and financial capacity.

Key benefits include:

- Fixed 5% markup for the first 10 years

- Loan tenure of up to 20 years

- Financing up to Rs. 10 million

- Up to 90% financing by banks

- No processing fee charged

- No penalty on early loan repayment

Eligibility Criteria for Applicants

This scheme is designed specifically for individuals who do not already own a house. The purpose is to ensure fairness and provide opportunities to those who genuinely need support. Many applicants, however, fail to qualify simply because they do not fully understand the eligibility requirements before applying.

In practical terms, the program targets first-time homebuyers who are currently living in rented houses or shared family homes. Both salaried individuals and self-employed persons can apply, provided they meet the necessary documentation and income requirements set by the participating financial institutions.

Basic eligibility conditions include:

- Must be a Pakistani citizen with a valid CNIC

- Should not own any house or apartment

- Must be a first-time homebuyer

- Applicable to both salaried and self-employed individuals

Available Financing Options Under the Scheme

The scheme offers multiple financing options, which makes it highly practical for a wide range of applicants. Instead of limiting people to a single type of loan, it allows them to choose according to their personal situation. This flexibility is one of the reasons why the program is gaining attention across the country.

For example, some families may already own a small plot but lack funds for construction. Others may want to buy a ready-made house to avoid the hassle of building. The scheme accommodates all such needs, ensuring that no deserving applicant is left out.

Financing options include:

- Purchase of a ready house or flat

- Purchase of plot with construction facility

- Construction on already owned land

- Apartment purchase up to 1500 square feet

Loan Structure and Monthly Installment Details

The loan structure has been carefully planned to balance affordability and long-term sustainability. For the first 10 years, borrowers pay a fixed markup of 5%, which significantly reduces monthly installments compared to market rates. This period is crucial because it allows families to stabilize their finances while gradually adjusting to loan repayment.

After the initial 10 years, the markup may shift to the prevailing market rate. However, by that stage, most borrowers are expected to have improved their financial position, making it easier to manage any increase in installments. This phased approach reflects a practical understanding of household financial growth over time.

Below is a simple table that gives an idea of expected monthly installments during the first 10 years:

| Loan Amount (PKR) | Estimated Monthly Installment (PKR) |

|---|---|

| 2,500,000 | 16,499 |

| 5,000,000 | 32,997 |

| 7,500,000 | 49,497 |

| 10,000,000 | 65,996 |

These figures provide a general understanding and may vary slightly depending on the bank’s policies and applicant profile.

Types of Financing Available

The program offers flexible housing solutions for different needs:

- Purchase of ready-made houses or apartments for immediate occupancy.

- Plot purchase with construction, enabling families to design their home.

- Construction of a new housing unit from scratch on land already owned.

Property scope includes:

- Houses up to 10 Marla.

- Apartments up to 1,500 sq. ft..

- Financing for partial or full construction, depending on your choice.

This flexibility allows families to select a plan that matches their budget, family size, and lifestyle

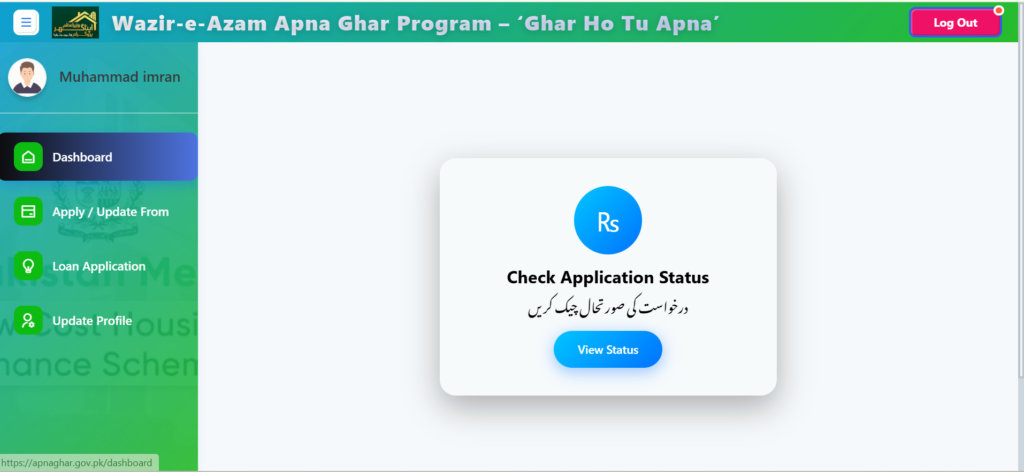

Step-by-Step Online Registration Process

The online portal simplifies the process:

- Create an account on apnaghar.gov.pk

- Log in if you are a returning user.

- Click Apply for Loan

- Fill in your details accurately, including CNIC, income, and property preferences.

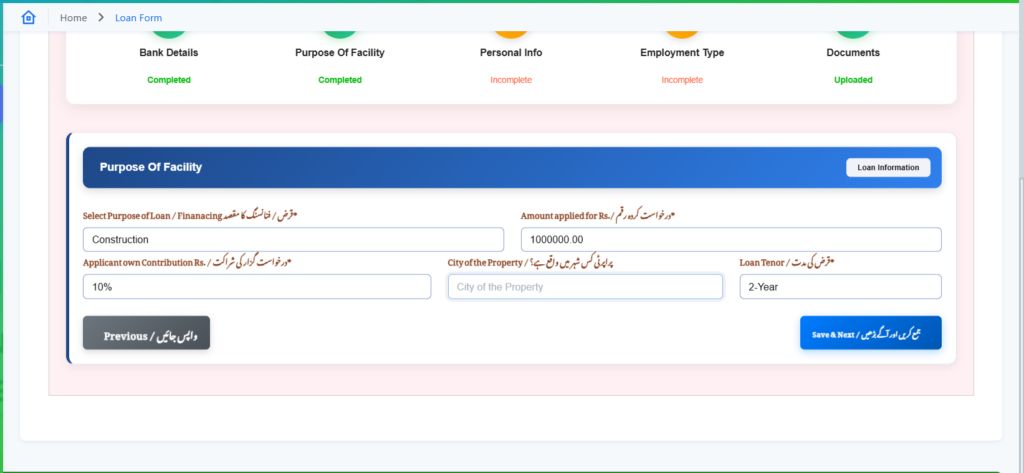

The first step is to provide complete bank details, such as the bank name, branch name, and city information.

Next, the applicant needs to provide personal details, including full name, CNIC number, contact information, and residential address.

Next, the applicant is required to provide employment and income details, including job status, monthly income, employer/business information, and any additional financial sources for loan assessment.

Next, the applicant must provide financial details, including monthly expenses, existing loan or card payments, and confirm whether they are an existing bank customer.

Tips for smooth registration:

- Keep all documents ready (CNIC, income proof).

- Ensure accuracy in all entries to prevent delays.

- Contact scheme representatives if guidance is needed.

Following these steps ensures a fast, efficient, and error-free application

Participating Banks and Financial Institutions

A major strength of this scheme is the wide network of participating financial institutions. Instead of relying on a single bank, the program includes commercial banks, Islamic banks, and microfinance institutions. This diversity increases accessibility and allows applicants to choose a bank they trust.

In real terms, this also improves approval chances because different banks have different evaluation criteria. If one bank rejects an application, another may approve it based on its own policies. This flexibility benefits applicants and strengthens the overall reach of the program.

Participating institutions include:

- Commercial banks such as HBL, UBL, MCB, Allied Bank

- Islamic banks like Meezan Bank and Bank Islami

- Microfinance banks including Khushhali and Mobilink

- House Building Finance Company (HBFC)

Loan-to-Value Ratio and Borrower Contribution

The program keeps initial payments low to make housing accessible:

- Banks cover 90% of the financing.

- Borrowers contribute only 10% of the total loan.

Benefits include:

- Reduced upfront costs.

- Encouragement for first-time buyers to invest.

- Maintaining cash flow for other family needs.

This structure ensures that families can own a home without excessive financial strain

Government Vision and Housing Targets

The government has set ambitious targets for this program, aiming to address Pakistan’s growing housing shortage. In the first year alone, the plan is to finance around 50,000 housing units, which reflects a serious commitment to solving the housing crisis. Over the next four years, the scale is expected to expand significantly with a multi-trillion rupee financing plan.

This initiative is not just about providing loans; it is part of a broader economic strategy. By promoting housing construction, the government is also supporting industries such as cement, steel, and labor, which play a key role in economic growth. From what I have seen, such programs can create a ripple effect that benefits multiple sectors simultaneously.

Why This Scheme Matters for Pakistani Families

For many families, rent is a constant financial burden that offers no long-term benefit. Month after month, a large portion of income is spent without building any asset. The Apna Ghar Program changes this equation by allowing families to invest in their own property instead of paying rent.

This shift has both financial and emotional value. Owning a home provides stability, security, and a sense of pride that renting cannot offer. It also ensures that future generations have a permanent place to live, reducing long-term financial stress.

Key impacts include:

- Reduction in housing shortage

- Promotion of home ownership culture

- Support for construction and related industries

- Creation of new employment opportunities

Important Guidelines for Applicants

Before applying, it is important to prepare properly and understand the requirements. Many applications face delays or rejection due to incomplete information or lack of documentation. Based on common experiences, careful preparation can significantly improve your chances of approval.

Applicants should also stay informed about the terms and conditions set by banks, as these may vary slightly. Regularly checking the status of your application ensures that you can respond quickly if additional information is required.

Important instructions include:

- Provide accurate and complete personal information

- Keep all required documents ready

- Understand bank-specific terms and conditions

- Monitor application status regularly

Official Resources and Contact Information

To avoid misinformation, it is always recommended to use official sources when applying or seeking guidance. The government has provided dedicated platforms and helplines to assist applicants throughout the process.

Official resources include:

- Website: www.apnaghar.gov.pk

- Website: www.pha.gov.pk

- UAN Helpline: 051-111-742-111

Final Thoughts

The Wazir Azam Apna Ghar Program 2026 stands out as one of the most practical housing initiatives introduced in recent years. It addresses real challenges faced by ordinary citizens and offers a clear path toward home ownership. From a journalist’s perspective, this scheme has the potential to bring meaningful change if implemented effectively and utilized wisely by the public.

For those who meet the eligibility criteria, this is more than just a loan opportunity—it is a chance to secure a better future. With proper understanding and timely application, many families can finally move closer to fulfilling their dream of owning a home.

FAQs

1. What is the Wazir Azam Apna Ghar Program 2026?

It is a government-backed housing finance scheme designed to help Pakistani citizens buy or build their own homes through low markup loans and easy installment plans. The program focuses on first-time homebuyers and aims to make housing affordable.

2. Who is eligible for the Apna Ghar Scheme?

Any Pakistani citizen with a valid CNIC who does not own a house or flat can apply. Both salaried individuals and self-employed persons are eligible, provided they meet the bank’s requirements.

3. What is the maximum loan amount available under this scheme?

Applicants can get a loan of up to Rs. 10 million, depending on their income, repayment capacity, and bank assessment.

4. What is the markup rate for the loan?

The markup rate is fixed at 5% for the first 10 years. After that, the remaining tenure will be based on the prevailing market rate.

5. What is the loan repayment period?

The repayment tenure can go up to 20 years, giving borrowers enough time to repay the loan in manageable installments.

6. Can I apply if I already own a plot?

Yes, you can apply for financing to construct a house on your already owned plot, as long as you do not own a constructed house or flat.

7. How can I apply for the Apna Ghar Program online?

You can apply by creating an account on the official portal, logging in, filling out the application form, and submitting it online.

8. Which banks are participating in this scheme?

Many institutions are part of the program, including commercial banks, Islamic banks, microfinance banks, and House Building Finance Company (HBFC).

9. Are there any processing fees or hidden charges?

No, the scheme does not include any processing fee, and there is no penalty for early loan repayment, making it more affordable for applicants.

10. How long does it take for loan approval?

The approval time depends on the bank and completeness of your application. If all documents are correct, the process can be completed within a few weeks, but delays may occur if information is missing.